Let’s break it down. A DSCR loan stands for Debt Service Coverage Ratio loan. It’s a type of real estate loan where the lender focuses more on the income produced by the property than your personal income. In other words, the key factor in approving this loan isn’t how much you make, but how much the property makes. This makes DSCR loans a go-to option for real estate investors—especially those with multiple income-generating properties or who might not have traditional W-2 income.

In a DSCR loan, lenders evaluate whether the property's income is sufficient to cover the loan payments. This is where the term “debt service” comes into play, referring to the amount needed to pay off both interest and principal on a loan. If the income from the property exceeds this debt service, then you’ve got a healthy DSCR, and you’re more likely to get approved.

So, in short: instead of scrutinizing your personal financials, lenders just want to see that the property pays for itself. Sound fair? It is, especially if you’re self-employed or scaling your rental portfolio fast.

Why are DSCR loans such a hot topic in the world of real estate and investment financing? Because they open up a world of opportunity for investors who might otherwise be sidelined by strict traditional mortgage rules.

In real estate, cash flow is king. A DSCR loan aligns perfectly with that mantra by focusing on the profitability of the investment. If your rental income outpaces your expenses—including mortgage payments—you’re seen as a low-risk borrower.

For business owners, DSCR is a crucial metric. It tells lenders whether your business generates enough cash to meet its debt obligations. So, whether you’re a landlord or a CEO, understanding DSCR is like having a flashlight in a dark cave—it guides your financial decisions and helps you avoid pitfalls.

Plus, DSCR loans can help speed up portfolio growth. Investors don’t have to wait for traditional lenders to comb through tax returns and pay stubs. Instead, they can scale faster by leveraging the income of the properties they already own.

In today’s competitive market, that’s a game-changer.

Let’s get the basics out of the way. DSCR stands for Debt Service Coverage Ratio. This financial metric is widely used by lenders, banks, and investors to assess a borrower's ability to repay a loan based on the income generated by a property or business.

Here’s how it breaks down:

So when you put it all together, the DSCR answers one simple question: Can the income from this property or business cover the cost of the loan payments?

This ratio is especially common in commercial lending and real estate investment, where the borrower’s income isn’t necessarily tied to a 9-to-5 job. Instead, the focus shifts to passive income, such as rent from tenants.

Understanding this term is crucial if you want to break into the world of real estate financing or business funding without getting bogged down in red tape. It’s the secret weapon smart investors use to secure funding with less personal financial scrutiny.

Now let’s put some real-world perspective on what a DSCR loan means financially.

If your DSCR is 1.0, it means your income just covers your loan payments—nothing more, nothing less. A DSCR above 1.0 means you have more income than debt obligations, which is a good sign for lenders. Below 1.0? That means your income falls short of your payments, and that’s a red flag.

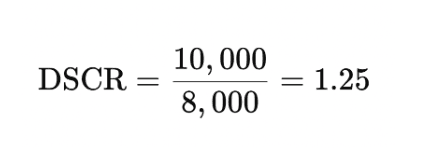

Here’s an example: if your rental property earns $10,000 a month and your total monthly loan payment is $8,000, your DSCR is:

A DSCR of 1.25 tells lenders you earn 25% more than you need to cover your loan.

Lenders typically look for a DSCR of at least 1.2 for safety, but some go as low as 1.0 for certain borrowers. This flexibility allows people with profitable properties but inconsistent personal income (think gig workers or entrepreneurs) to still access real estate loans.

So, if you’re tired of being turned down for loans just because of your tax returns, this could be your golden ticket.

Alright, let’s get into the math. The formula for DSCR is straightforward:

Here’s what each part means:

Let’s break that down with an example. Say you have:

Your annual NOI = ($12,000 - $4,000) * 12 = $96,000

Your Total Debt Service = $80,000

So your DSCR = $96,000 / $80,000 = 1.2

This means you’re earning 20% more than your loan requires—which is often the magic number lenders love to see.

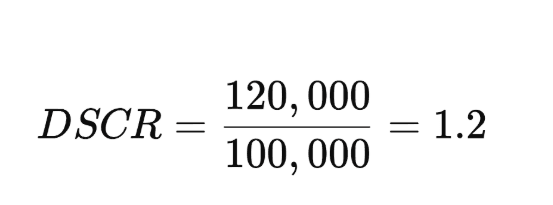

To make this even clearer, let’s walk through a step-by-step example of how to calculate your DSCR.

Step 1: Determine your gross rental income

Let’s say you earn $15,000 per month = $180,000 per year

Step 2: Subtract operating expenses (excluding mortgage)

Let’s say annual expenses total $60,000

Net Operating Income = $180,000 - $60,000 = $120,000

Step 3: Find your annual mortgage obligation

Let’s say your mortgage payments total $100,000 per year

Step 4: Plug into the DSCR formula

Now comes the big question: what’s a good DSCR? What do lenders actually want?

Generally speaking:

Different lenders have different thresholds, and riskier borrowers may be required to meet higher ratios. A safer bet is to aim for at least 1.25 to keep your options wide open and avoid getting hit with high interest rates or loan rejections.

Want to boost your DSCR? Improve your cash flow, reduce operating expenses, or look for cheaper financing terms. It’s that simple.

DSCR loans are a cornerstone in the commercial real estate world. Why? Because commercial deals are all about income. Think of office buildings, retail spaces, warehouses, or multifamily properties—these aren't just places to live or work; they're income-generating machines. Lenders want to know one thing: can this property pay for itself?

With commercial DSCR loans, your personal financial background takes a backseat. Instead, the spotlight is on the net operating income (NOI) of the property. If that NOI comfortably covers your debt payments, you’re good to go.

These loans are especially useful for:

Commercial DSCR loans usually require higher DSCR ratios (often 1.25 or more), larger down payments (20–30%), and detailed property analysis. But the tradeoff is worth it: faster approvals, less red tape, and a funding method that scales with your ambitions.

Now here’s where DSCR loans really shine for small-scale investors and landlords. Residential DSCR loans are perfect if you're buying a single-family rental, duplex, or even a short-term rental like an Airbnb. If you’ve got consistent cash flow and the property produces enough income, you don’t need to show tax returns, W2s, or pay stubs.

This is a big deal for self-employed folks, side hustlers, or anyone whose personal income looks “irregular” on paper. The property’s income is what counts.

Let’s say you’re buying a duplex that brings in $3,000/month in rent. Your mortgage payment is $2,200/month. That’s a DSCR of 1.36, which is solid. You could get approved for a loan even if your personal income is unpredictable.

Lenders will still check your credit score, reserves, and down payment (usually 20–25%), but the focus remains on the property. This gives real estate investors a way to scale fast—without letting traditional income requirements slow them down.

So how do DSCR loans compare to the regular mortgages most people are used to? Let’s break it down:

| Feature | DSCR Loan | Traditional Loan |

| Income Verification | Based on property income | Based on personal income |

| Paperwork | Less intensive | Tax returns, W2s, bank statements required |

| Speed | Faster approval process | Longer underwriting time |

| Use Case | Investment properties | Primary residences or some rentals |

| Credit Score Impact | Still considered, but less important | Very important |

| Down Payment | 20–30% typically | Can be as low as 3–5% for first-timers |

In essence, DSCR loans are all about leverage and speed. They work best when you’re focused on cash-flowing rental properties or scaling a portfolio. Traditional loans are better suited for homebuyers looking to live in the property or who need lower down payments.

If you’re building a business around real estate, DSCR loans are the turbo boost. But if you’re buying your first home to live in, stick with conventional or FHA loans for better rates and terms.

Let’s be real—traditional mortgages can feel like an IRS audit. You’ve got to hand over W2s, tax returns, pay stubs, bank statements, and explain every dollar you’ve ever made. It’s exhausting.

DSCR loans flip that script. No income verification needed.

If your property cash flows, that’s what matters. This is a lifesaver for:

With DSCR loans, you skip the headache and get straight to the deal. This makes it possible to finance rental properties without jumping through bureaucratic hoops. It’s efficient, investor-friendly, and frankly, long overdue in the lending world.

DSCR loans are like the Swiss Army knife of real estate financing. They adapt to your needs, especially if you're growing a portfolio or running a business. Unlike conventional mortgages that penalize you for having too many properties, DSCR lenders often welcome experienced investors.

You can:

This flexibility means more options, faster scaling, and better alignment with real estate investing goals. Entrepreneurs and full-time investors thrive with DSCR loans because they don’t have to fight the system—they work with it.

And because these loans are built around cash flow, the better your properties perform, the more financing you can access. It’s a performance-driven system, not a paperwork-driven one.

Here’s the good news: DSCR loans aren’t as credit-score obsessed as traditional mortgages. You don’t need an 800 FICO to qualify. Many lenders will work with scores as low as 620–640, though the best rates typically come with scores of 700+.

Even if your score isn’t perfect, as long as your property cash flows well, you’ve still got a shot.

That said, credit still matters. A higher score can:

But if your credit is shaky, don’t panic. Some DSCR lenders specialize in working with credit-challenged investors—as long as the deal makes financial sense.

So if you’ve had a bankruptcy, foreclosure, or just a few late payments, DSCR loans might be more forgiving than the traditional route.

When it comes to qualifying for a DSCR loan, the most critical metric is—you guessed it—the DSCR ratio itself. Lenders typically set a minimum DSCR requirement to ensure the property is generating enough income to cover the debt obligation with a buffer.

So, what’s the magic number? Most lenders want to see a DSCR of at least 1.2. This means the property earns 20% more income than what’s needed to make monthly loan payments. However, the threshold can vary:

Keep in mind: The higher your DSCR, the more confident the lender will be that you can repay the loan, making it easier to get approved and secure better terms.

To qualify, you’ll need to provide:

The stronger your DSCR, the better your chances of approval, regardless of your personal income or credit quirks.

This is where the rubber meets the road. To qualify for a DSCR loan, your property needs to cash flow positively—period.

Here’s what lenders evaluate:

To make the cut, your NOI must be higher than your debt service—ideally by 20% or more.

Pro tip: If your property’s DSCR is below the required threshold, you can often improve it by:

Cash flow is king in this game. Make sure your investment works on paper before applying, because that’s how your lender will judge it.

While DSCR loans are more flexible in some areas, they still require some skin in the game. Expect to put down 20% to 30%, depending on:

That’s right—there are no zero-down DSCR loans. Lenders want you to have a financial stake in the property to reduce their risk.

Additional requirements often include:

These requirements are designed to ensure you’re financially capable, but they’re way less invasive than traditional mortgages that want to see your entire financial history. If you’re an investor with cash, decent credit, and a cash-flowing property, you’re already halfway there.

DSCR loans aren’t always the cheapest form of financing. Since lenders are taking a risk by relying solely on property income (not your personal income), they usually charge higher interest rates than traditional loans.

Typical rates can be 1–2% higher than a conventional mortgage. That might not sound like much, but on a large loan, it adds up quickly.

What impacts the rate?

While the speed and flexibility of DSCR loans are huge advantages, you’ll need to weigh that against the long-term cost. If you plan to hold the property for a long time, refinancing into a lower-rate loan later might be a smart move once your personal income stabilizes or credit improves.

It’s a classic case of “you get what you pay for”—convenience at a slightly higher cost.

DSCR loans are based on property income, which can fluctuate—especially in changing markets. Think about short-term rentals (Airbnb), commercial leases, or even long-term tenants during a recession.

If rents drop or your unit sits vacant for a while, your DSCR can take a hit. And if your income dips below your debt service? You could default on the loan or face challenges refinancing.

This makes market analysis crucial. Before jumping into a DSCR loan, ask:

Also, keep an emergency fund. Even a few months of vacancy can throw your DSCR ratio off track.

DSCR loans offer speed and scalability, but they don’t come without risk. Make sure you’re investing in a solid market and managing your property smartly.

Because DSCR loans don’t require personal income verification, they’re considered non-QM (Non-Qualified Mortgages)—which puts them in a higher-risk category.

If your property’s income drops significantly, and you can’t cover the loan payments out-of-pocket, lenders have limited recourse. That’s why DSCR loans often come with:

Because DSCR loans don’t require personal income verification, they’re considered non-QM (Non-Qualified Mortgages)—which puts them in a higher-risk category.

If your property’s income drops significantly, and you can’t cover the loan payments out-of-pocket, lenders have limited recourse. That’s why DSCR loans often come with:

The risk of default is real, especially for investors relying entirely on passive income. That’s why it’s essential to:

Treat a DSCR loan like any investment—do your due diligence, plan for contingencies, and never assume everything will go perfectly.

Want a better DSCR? Boost your Net Operating Income (NOI). Here's how:

The more you make, the stronger your DSCR—and the easier it becomes to refinance, pull cash out, or acquire more properties.

On the flip side, decreasing your loan costs also boosts DSCR. Try this:

Less debt = higher DSCR. Even if you can’t raise rent right away, slashing your debt service gives you more breathing room—and more leverage with lenders.

How you manage your property impacts everything—from cash flow to expenses to tenant retention. Strategic property management helps increase income and reduce unnecessary costs.

Tips:

A DSCR loan is more than just another loan product—it’s a gateway to scalable, efficient, and investor-friendly real estate financing. Whether you're growing your rental portfolio, launching a short-term rental business, or just looking for a smarter way to leverage income-producing properties, DSCR loans offer unmatched flexibility and speed.

At Cornerstone Mortgage Group, we understand that your portfolio’s cash flow should speak louder than your paystubs. That’s why we’ve built a streamlined DSCR loan program that puts your property performance front and center. With competitive rates, expert support, and fast closings, we help real estate investors move quickly and confidently, without getting bogged down in paperwork.

Ready to finance your next investment property the smart way? Let’s make it happen.

Real estate investors, business owners, and self-employed borrowers who want to qualify based on rental income—not personal income. It’s an ideal option for those scaling portfolios or with non-traditional income.

Absolutely. At Cornerstone Mortgage Group, we offer DSCR loan solutions for both long-term and short-term rentals. We assess income based on rental history or market projections—even Airbnb revenue.

Our DSCR loan process is designed for speed. Pre-approval can take as little as 24–48 hours, and we typically close in 2–3 weeks, depending on the complexity of the deal.

We work with a wide range of credit profiles, with minimum scores starting around 620. That said, higher scores and stronger DSCR ratios can unlock better terms and rates.

Getting started is easy. Contact our investment loan specialists today for a free consultation and customized quote. We’ll help you evaluate your property’s cash flow and guide you through every step of the process.